The 1921 Tulsa Race Massacre and the Insurance Denials That Followed

**Brief Description** This article explores how many insurance companies denied claims after the 1921 Tulsa Race Massacre destroyed the Greenwood District. Using riot clauses in policy contracts, insurers refused compensation to Black property owners who had lost homes and businesses. Drawing on insurance records, court filings, and Oklahoma state investigations, the piece examines how these denials deepened the economic damage and slowed the rebuilding of the once-thriving community.

6/12/20262 min read

The 1921 Tulsa Race Massacre and the Insurance Denials That Followed

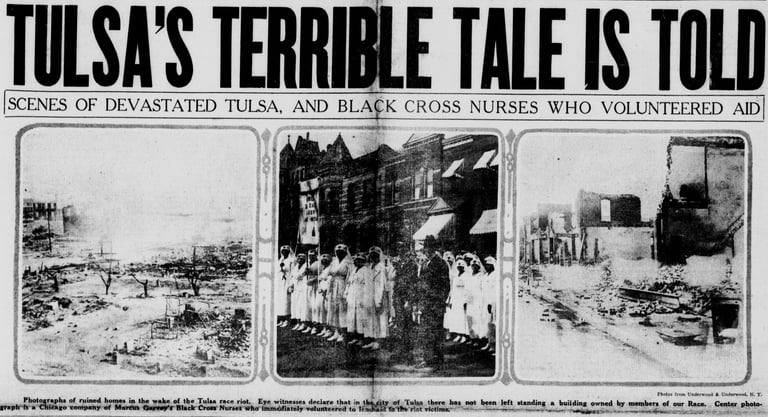

In late May and early June of 1921, the Greenwood District of Tulsa, Oklahoma—often called “Black Wall Street”—was devastated by one of the most destructive episodes of racial violence in United States history. Greenwood had been a thriving community with banks, theaters, medical offices, hotels, and hundreds of Black-owned businesses. Within less than two days, much of the district was burned to the ground.

Historians estimate that more than 30 city blocks were destroyed. Thousands of residents were left homeless, and many businesses were reduced to ashes. While the violence itself caused immediate devastation, another form of loss followed in the aftermath: the denial of insurance claims filed by Black property owners.

Many Greenwood residents had carried insurance policies to protect their homes and businesses. However, when they attempted to file claims after the destruction, insurance companies frequently refused to pay. A key reason was the use of “riot clauses” contained in many policies. These provisions allowed insurers to deny compensation if property damage occurred during a riot or civil disturbance.

Insurance companies argued that the destruction of Greenwood fell under these riot exclusions. As a result, numerous claims submitted by Black residents were rejected. For individuals and families who had already lost everything, these denials made rebuilding nearly impossible.

Court filings from the period show that some residents attempted to challenge these denials legally. Lawsuits were filed against insurers in hopes of recovering damages, but most efforts were unsuccessful. Without financial support from insurance payouts, rebuilding efforts relied largely on personal resources, community cooperation, and determination.

The denial of insurance compensation compounded the economic consequences of the massacre. Greenwood had been one of the most prosperous Black communities in the country, and the destruction of homes, offices, and commercial property erased generations of wealth and opportunity.

Evidence of these insurance denials exists in archived claim records, legal filings, and investigative reports. Oklahoma state investigations conducted decades later examined the destruction and the economic losses suffered by Greenwood residents. These reports confirmed that insurance refusals were widespread and played a major role in the community’s slow recovery.

Today, historians continue to examine these documents to understand the full economic impact of the Tulsa Race Massacre. Insurance records, court cases, and state investigations reveal that the aftermath of the violence extended far beyond the fires themselves. Financial barriers—created through policy language and legal rulings—made rebuilding extraordinarily difficult.

The paper trail remains preserved in insurance archives, court records, and state investigative reports. These documents help explain why the destruction of Greenwood had consequences that lasted for generations.

Proof Trail: Insurance claim records, Oklahoma state investigative reports, and court filings related to property loss following the 1921 Tulsa Race Massacre.